Infographic: The January Reset

Coverage Changes Every Year

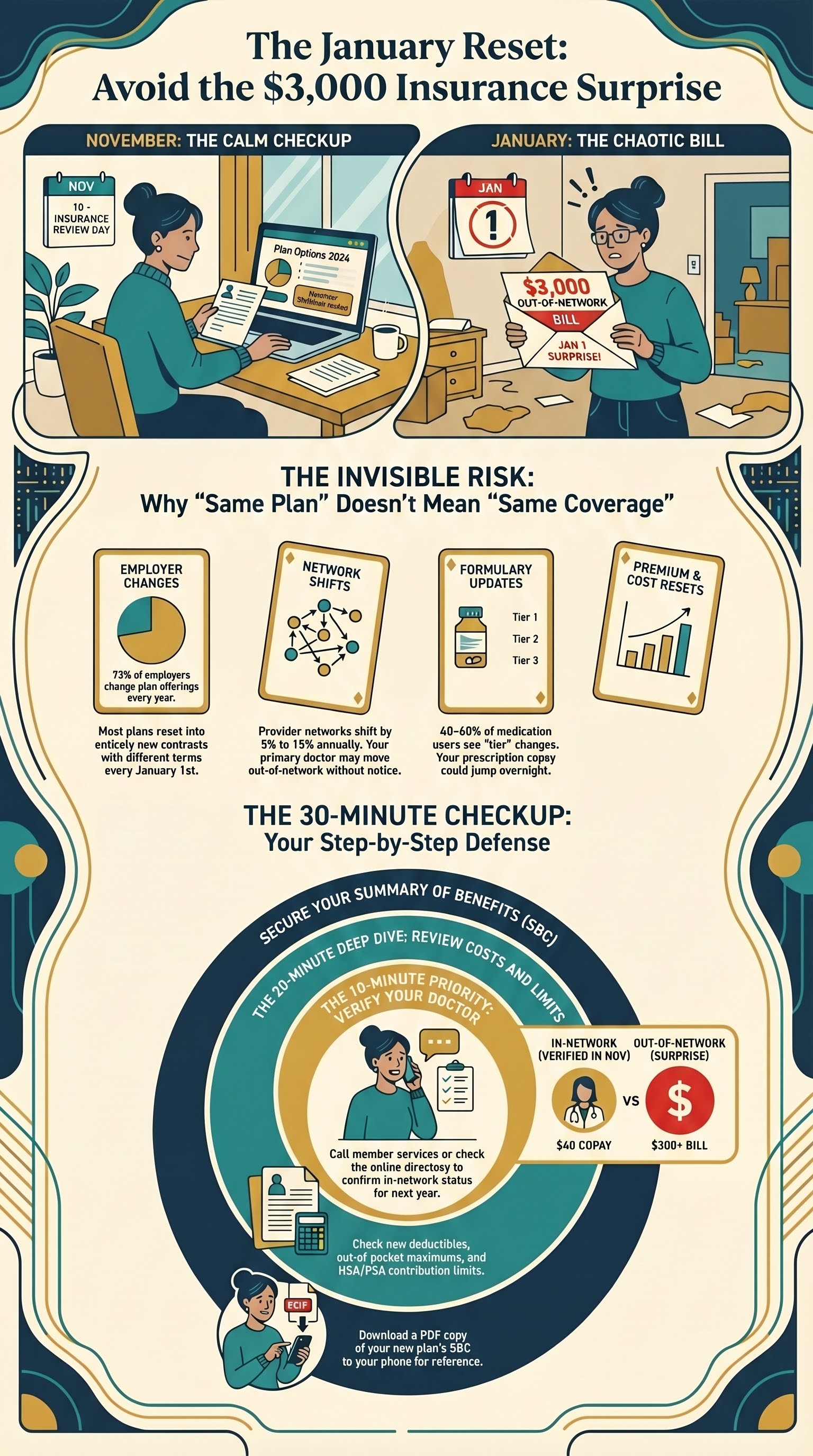

You have an annual physical to catch health problems before they become emergencies. Your health insurance needs an annual checkup too. Right now, your coverage is probably different from what it was a year ago. Your deductible reset on January 1. Your medication list on your plan may have changed. The hospital you’ve been going to might be out-of-network now. And you won’t know any of this until you try to use your insurance — and by then, it’s too late to switch. An annual coverage checkup is how you catch these changes before they cost you money.

Why Plans Change Every Year

Here’s what changes every year. Three-quarters of employers modify their health plan offerings annually. That could mean your copay for a doctor visit went up, or your deductible increased. For people on Medicare or marketplace plans, the changes are built into the system — new benefits take effect January 1 every year.

Medications are a huge one. Your plan’s list of covered medications (called the formulary) changes every single year. A medication you’ve been taking that was in Tier 1 (cheapest copay) might move to Tier 3 (expensive copay). Or it might be removed from the formulary entirely, and you’ll need prior authorization or a different drug. This happens to 40 to 60 percent of people taking maintenance medications annually.

Networks change too. The hospitals and doctors in your plan’s network shift every year. A hospital you’ve been using might drop out of network. Your primary care doctor might leave the network. You won’t know until you call to schedule an appointment and they tell you you’re out-of-network.

Your deductible resets January 1. Your out-of-pocket maximum resets. If you have an HSA or FSA, contribution limits might change (and FSA rules mean use-it-or-lose-it). These aren’t decisions you need to make — they happen automatically. But you need to know the new numbers.

Open Enrollment Period is your window to change plans. For Medicare, it’s October 15 to December 7. For marketplace plans, it’s November 1 to January 15. For employer plans, it’s typically a 30 to 45-day window in the fall or winter. The changes take effect January 1. If you don’t review your coverage by November, you’ve missed the window.

The Numbers Show Why This Matters

Here’s why you can’t skip this. Kaiser Family Foundation data shows that 73 percent of employers change their health plan offerings year to year. For people with chronic conditions on maintenance medications, formulary churn is real: 40 to 60 percent of medication users experience a tier change or loss of coverage every year.

In-network networks shift too. Provider networks change by 5 to 15 percent annually — hospitals and doctors moving in and out. If you don’t verify your primary doctor is still in-network, you could show up to an annual visit and discover you’re out-of-network.

The Protection Score you calculated in the last lesson is only accurate if your coverage information is current. If your deductible went up by $500 and you didn’t know it, your protection score is wrong. If your medication isn’t on your formulary anymore, your out-of-pocket costs are wrong. An outdated protection score doesn’t protect you — it just makes you feel secure when you aren’t.

The tax year interaction is another reason to verify. HSA contribution limits change annually. FSA funds don’t roll over (use-it-or-lose-it). If you don’t verify your HSA or FSA contributions and balances by year-end, you could lose money.

Your Seven-Item Checkup

Here’s your annual checkup. This is a seven-item checklist. Schedule 30 minutes in November — before the Open Enrollment deadline. Go through each one:

If you can’t find this information on your plan’s website, call member services (the number is on your insurance card) and ask them to mail you the documents.

Timing Framework: The Annual Calendar

Insurance Isn’t Static — So Your Review Can’t Be Either

Your health insurance isn’t static — it’s a contract that resets every year. You wouldn’t ignore changes to your health; don’t ignore changes to your coverage. An annual checkup takes 30 minutes and saves you hundreds of dollars. Next lesson, we’ll put together a resource toolkit — everything you need when something goes wrong with your claim.

Schedule Your Annual Review

Get a reminder to do your annual insurance checkup. We’ll send you a checklist and calendar block in September.

Evidence: Sources for This Lesson

About This Lesson

You’re 83% through Module 5: Your Safety Net. This lesson teaches the annual insurance checkup as a lifelong habit, not a one-time task. The seven-item checklist is designed to be completed in one sitting, once per year, by any patient on any plan type.

Maria (our patient on an employer plan) will use this to verify her medications stay in Tier 1. James (post-denial and rebuilding) will use this to ensure his appeals don’t lapse. Priya (on marketplace coverage) will use this to compare plans during Open Enrollment. One lesson, three lives, one habit.

This lesson is part of How Your Insurance Actually Works—an evidence-based course designed with clinical expertise by the AnchorWellPress Medical Team. This content is for informational purposes only and does not constitute medical advice, diagnosis, or treatment. Always consult your healthcare provider.

Check Your Understanding

It’s early November. Your plan from last year auto-renews on January 1. What’s the single most important thing to verify during your 30-minute November checkup?

Do This Now

Today, 10 minutes: look up your primary-care doctor on your insurance plan’s website, or call member services (back of your card), and confirm they are in-network for next year. One tier change or network drop can cost you $3,000.

Then install the habit: open your calendar and block 30 minutes on the second Saturday of November titled “Insurance Checkup.” That one recurring appointment each year is the difference between being caught off-guard and being in control.

Walking into open enrollment? Start with the Benefits Quiz →