Infographic: Open Enrollment Explained

The Decision Point

Every year, your insurance company sends you a piece of paper that says “Open Enrollment Period.” And every year, most people ignore it. They think: “I’ll just keep the same plan I have.” But here’s what that paper is really saying: “Everything about your health insurance has changed. Your choices, your costs, your doctors, your medications — all of it is different now. You get to decide what to do about that.” This lesson is about making that decision in one hour, not one year.

Three Different Calendars

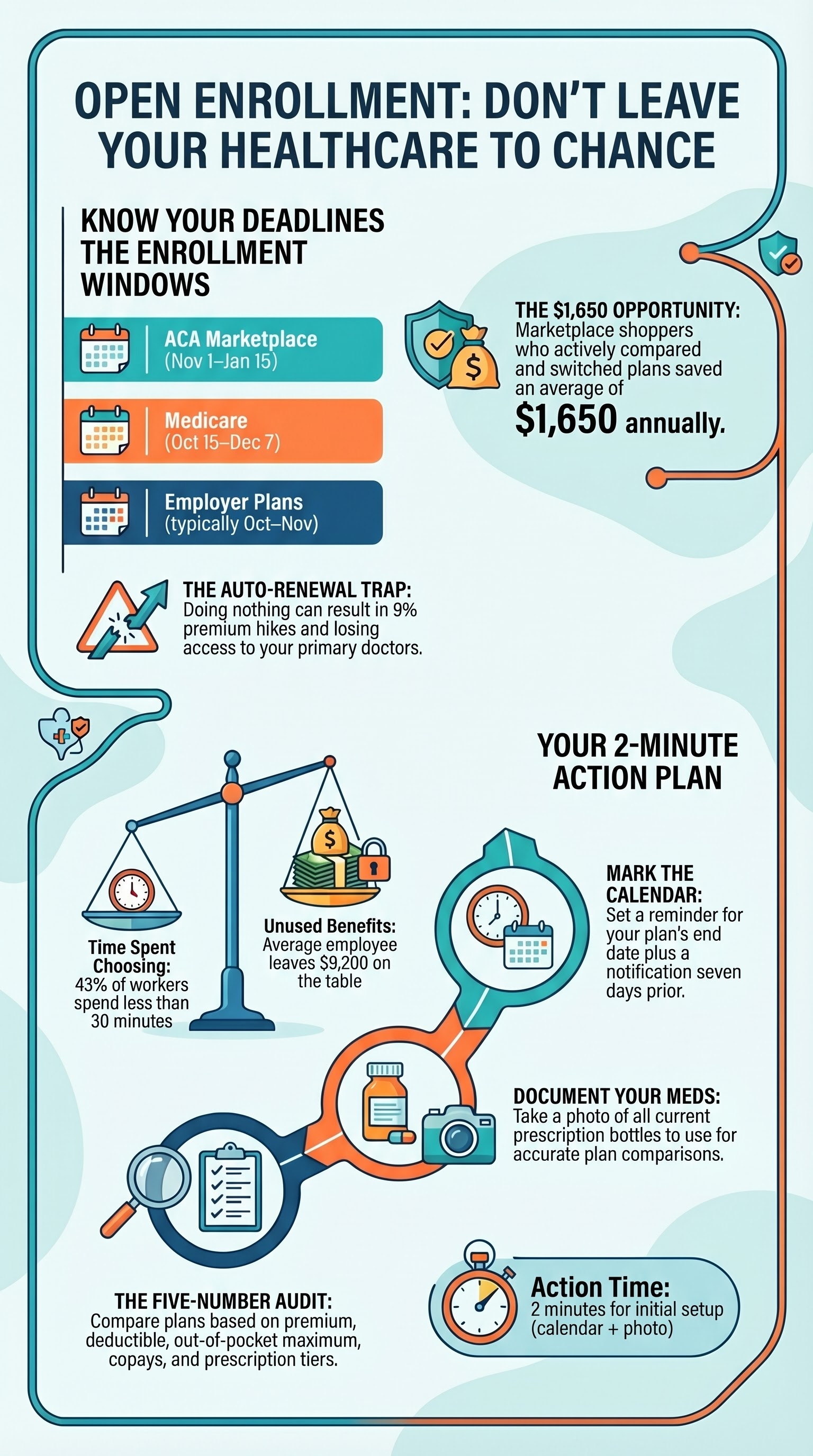

Open enrollment happens at different times, depending on where you get your insurance.

Medicaid is different: Medicaid doesn’t have a single “open enrollment period.” You can apply or change your coverage year-round, based on income changes.

The reason all these windows exist is that insurance costs and coverage change every single year. Your old plan is not your old plan anymore. The network of doctors might have changed. The medications covered might have changed. The premium definitely changed. So every year, you get a decision point. Most people use it to do nothing — they accept the default. But you don’t have to.

The Six Numbers That Matter

When comparing plans, there are six things that actually matter. Here’s the framework:

The temptation is to pick the cheapest premium. But the cheapest premium often means a higher deductible. If you have a chronic condition and fill prescriptions regularly, the copay structure matters more than the monthly premium. If you have a specific doctor you want to see, network matters. If you take a specific medication, formulary matters. No single plan wins on all six. You’re trading off.

Your Five-Step Plan

Here’s your action this week. Build one simple plan comparison sheet. Here’s how:

Need help? Two resources exist:

Full Lesson Transcript

Every year, your insurance company sends you a piece of paper that says “Open Enrollment Period.” And every year, most people ignore it. They think: “I’ll just keep the same plan I have.” But here’s what that paper is really saying: “Everything about your health insurance has changed. Your choices, your costs, your doctors, your medications — all of it is different now. You get to decide what to do about that.” This lesson is about making that decision in one hour, not one year. Let’s start.

Open enrollment is different for everyone. If you get coverage through the Marketplace, your window is November 1 through January 15 — ten weeks to enroll, switch plans, or drop coverage. If you’re on Medicare, your window is October 15 through December 7. If you get insurance through an employer, open enrollment usually happens in October or November and lasts 30 to 60 days. Medicaid is different — there’s no annual window. You can apply or change coverage year-round. The reason these windows exist is that insurance costs and coverage change every single year. Your old plan is not your old plan anymore.

When comparing plans, there are six things that matter. One: the premium, the monthly cost. Two: the deductible, what you pay before the plan starts paying. Three: the copay and coinsurance, your share of each visit or prescription. Four: the out-of-pocket maximum, the ceiling for how much you’ll pay in a year. In 2025, that federal ceiling is $9,100 for individual coverage. Five: the network, which doctors and hospitals your plan covers. And six: the formulary, which medications are covered and at what cost. The temptation is to pick the cheapest premium. But the cheapest premium often means a higher deductible. No single plan wins on all six. You’re trading off.

Here’s your action this week. Build one simple plan comparison sheet. First, get your open enrollment notice. Second, list your current medications. Third, get your three top plan options and write down the premium, deductible, copay, out-of-pocket max, and whether your doctor is in network. Fourth, check each plan’s formulary and see where your medications are covered. Fifth, compare. Is the cheapest plan actually the cheapest? Is your doctor in the network? Are your medications covered? If the answer to all three is yes, you have a real option. Your plan’s member services line can help you, or use the tool at healthcare.gov.

Open enrollment isn’t random. It’s the annual decision point where you get to see what’s changed, compare your options, and choose intentionally. Most people ignore it. You’re not going to be most people. You’re going to spend one hour this week with your plan comparison sheet. You’re going to know, not guess. Next lesson, we’ll look at what to do if your claim gets denied. See you there.

Get Your Plan Comparison Template

Download a free worksheet to organize the six factors and compare your plan options side-by-side.

Sources & References

Check Your Understanding

Priya missed her window to change plans. Her old employer plan no longer covers her GLP-1 medication, so she’s paying $1,100 out of pocket every month. When can she switch plans?

Do This Now

Pull out your calendar right now and write down your open enrollment end date — for ACA plans it’s January 15; for employer plans it varies. Then list the three medications and one specialist you used most this year. Those five pieces of information are what you’ll compare every plan against this week.

Find out which plan type fits your situation with the Benefits Quiz →About This Lesson

Course: How Your Insurance Actually Works (Insurance IQ)

Module: 4 · Choosing Your Plan

Lesson: 4.1 · Open Enrollment Playbook

Learning Goal: By the end of this lesson, you will be able to identify your specific open enrollment window, compare insurance plans using six key factors, and make an intentional plan choice before the deadline.

Persona: Maria, making decisions about next year’s coverage

Video Length: 6–7 minutes

Need Help? Discuss this lesson with your healthcare provider or contact your plan’s member services line.

This lesson is part of How Your Insurance Actually Works—an evidence-based course designed with clinical expertise by the AnchorWellPress Medical Team. This content is for informational purposes only and does not constitute medical advice, diagnosis, or treatment. Always consult your healthcare provider.