See It In Action: The Same Denial, Different Rights

Two patients with identical insurance cards receive the same denial. But their paths to resolution are completely different:

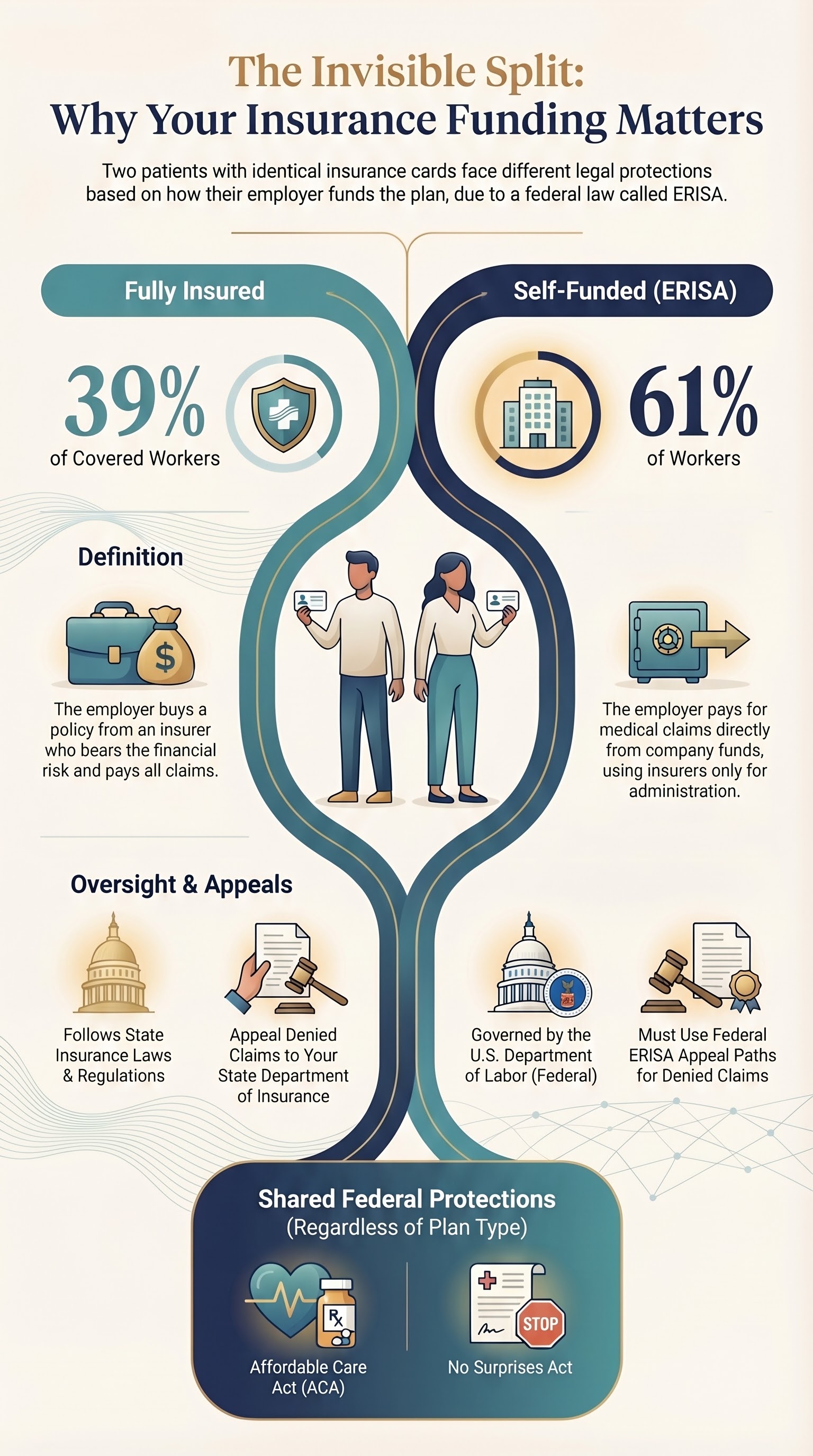

Sarah: Fully Insured Plan

Plan Type: Blue Cross fully insured plan

Employer: Small business (50 employees)

Claim: Knee surgery denied as “not medically necessary”

Her Path: Files complaint with her state Department of Insurance

Outcome: State DOI investigates, determines denial was improper, orders Blue Cross to pay

Her Rights Are Protected By: State law (her state’s insurance regulations), state benefit mandates (coverage requirements for specific treatments)

James: Self-Funded ERISA Plan

Plan Type: Blue Cross administered, company-funded plan

Employer: Large corporation (5,000 employees)

Claim: Identical knee surgery denied as “not medically necessary”

His Path: State DOI tells him they have no authority; he must contact U.S. Department of Labor

Outcome: DOL has a different process and timeline; state benefit mandates do not apply

His Protections Are Under: Federal law only (ERISA); state laws are preempted. State benefit mandates do not apply to his plan.

The Card Looks the Same. The Law Is Completely Different. Both patients have “Blue Cross” on their insurance card. Both received a denial for the same procedure at the same hospital. But which legal system applies to each of them depends on a single question about how their employer funds the plan.

Check Your Understanding

Knowledge Check

If your employer self-funds your health plan, which agency oversees your insurance complaints?

Not quite. ERISA preempts state insurance laws for self-funded plans. The primary federal regulator is the U.S. Department of Labor, which oversees ERISA compliance. Your state’s Department of Insurance does not have jurisdiction over self-funded ERISA plans.

Do This Now

Ask your HR department one question: “Is our health plan self-funded or fully insured?” Write down the answer. It determines which complaint channels apply to you, which consumer protections cover you, and which appeal paths are available if you ever face a claim denial.

About This Lesson

This lesson is part of How Your Insurance Actually Works — an evidence-based course designed with clinical expertise by the AnchorWellPress medical team. This content is for educational purposes only and does not constitute medical advice, diagnosis, or treatment. Always consult your healthcare provider.

This content is for informational purposes only and does not constitute medical advice, diagnosis, or treatment. Always consult your healthcare provider before making any health decisions.