You just lost your job. Or you got married. Or you had a baby. Most people think they're stuck with their old insurance until next open enrollment—sometimes months away. They're not.

Here's something I wish every patient knew: when your life changes, the insurance door opens again. You get a second chance to change plans. The system calls it a Special Enrollment Period. You call it: I have 60 days to pick something better.

How the System Works

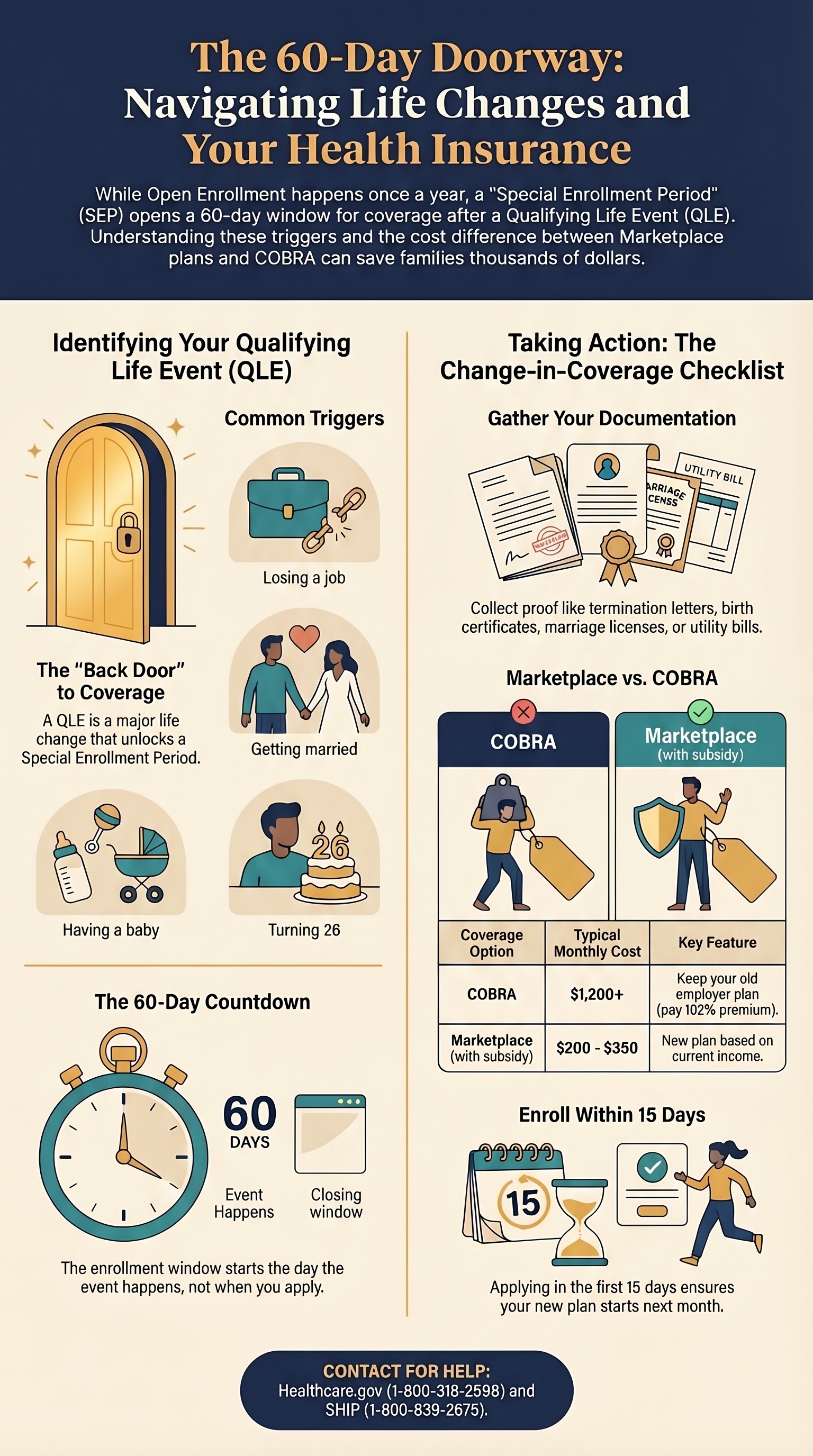

The regular way to enroll in health insurance is during open enrollment—usually just once a year in November and December. The insurance system locks the door the rest of the time. But the system also recognizes that life doesn’t wait for open enrollment. So it built in a back door: the Special Enrollment Period (SEP).

An SEP opens when something big happens in your life. We call it a "Qualifying Life Event," or QLE. The list is longer than you think:

- You lose your job and your health insurance goes away

- You get married

- You have a baby or adopt

- You move to a new state where different plans are available

- Your income changes enough to affect your subsidy

- You turn 26 and age off your parent’s plan

- You lose Medicaid coverage

- You graduate from a student health plan

Any of these events pulls the door open.

COBRA: An Alternative You Should Know About

If you also lost health insurance with your life change—like losing employer coverage when you get laid off—you might hear about COBRA. COBRA lets you keep your old employer plan for up to 18 months. But COBRA costs 102 percent of the full premium. You pay both the employee and employer share. That’s often $800, $1,500, $2,000 a month or more.

Meanwhile, you can enroll in a marketplace plan and get a subsidy that might bring your cost down to $200 or $300 a month. Same coverage. Very different costs. That’s why knowing about the SEP matters.

Three Life Changes. Three 60-Day Windows.

Maria: Job Loss

Maria is 42 and loses her job. Her employer coverage ends on the 15th. That’s her Qualifying Life Event—loss of coverage. She has 60 days from the 15th to enroll in marketplace coverage or another employer plan. She also just lost income, which is another QLE: change in income.

Because she enrolls within 15 days of her job loss, her new marketplace plan starts on the first of the next month. She checks healthcare.gov, finds plans, compares them using the framework from our previous lesson, and picks one. Cost: $350 a month with subsidies. COBRA would have been $1,200.

James: Aging Off Parent Plan

James just turned 26. His parent’s plan covers him through the end of the month. On his 26th birthday, he ages off—that’s a QLE. He has 60 days from his birthday to enroll. He waits 40 days (procrastination happens), then enrolls in the marketplace. His coverage starts on the first of the following month—20 days after enrollment. Close call, but he made it.

Priya: New Baby

Priya has a baby in April. That’s her QLE. She has 60 days from the baby’s birth to add the baby to her existing plan or enroll in a new plan. She requests a retroactive effective date, and her coverage for the baby can go back to the birth date. She keeps her existing plan and adds the baby. Clock: she has 60 days to make the call.

Your Action This Week

Keep this "Change in Coverage Checklist" in your phone. The day something happens—you lose your job, you get married, you have a baby—you pull up this list. You have 60 days from that day. Here’s what you do:

Change in Coverage Checklist

If the process is confusing or you miss a deadline, your state has free help. Ask for SHIP (State Health Insurance Assistance Program) at 1-800-839-2675. They help you navigate enrollment and compare plans.

Get the Change in Coverage Checklist

Download your printable checklist to keep in your phone for the moment life shifts.

About This Lesson

This lesson is part of How Your Insurance Actually Works—an evidence-based course designed with clinical expertise by the AnchorWellPress Medical Team. This content is for informational purposes only and does not constitute medical advice, diagnosis, or treatment. Always consult your healthcare provider.

Check Your Understanding

Maria got married last Tuesday. She wants to join her husband’s health plan. How much time does she have to make the switch before she has to wait until next open enrollment?

Do This Now

If you’ve had a qualifying life event in the last 60 days, open your phone calendar right now and set a reminder for Day 50 and Day 55 from the event date. The 60-day clock does not pause for holidays, illness, or confusion. Missing this window means waiting a full year.

Not sure which plan to choose? Try the Benefits Quiz →Infographic: The 60-Day Doorway